There’s a quiet tension that most financially disciplined people never talk about openly: the guilt that comes with spending money on fun. Whether it’s a spontaneous weekend getaway, a night at a high-end restaurant, or a session on a gaming platform, discretionary spending often feels like a betrayal of your wealth goals – especially when you’ve spent years fine-tuning your portfolio, automating your savings, and optimizing your tax strategy.

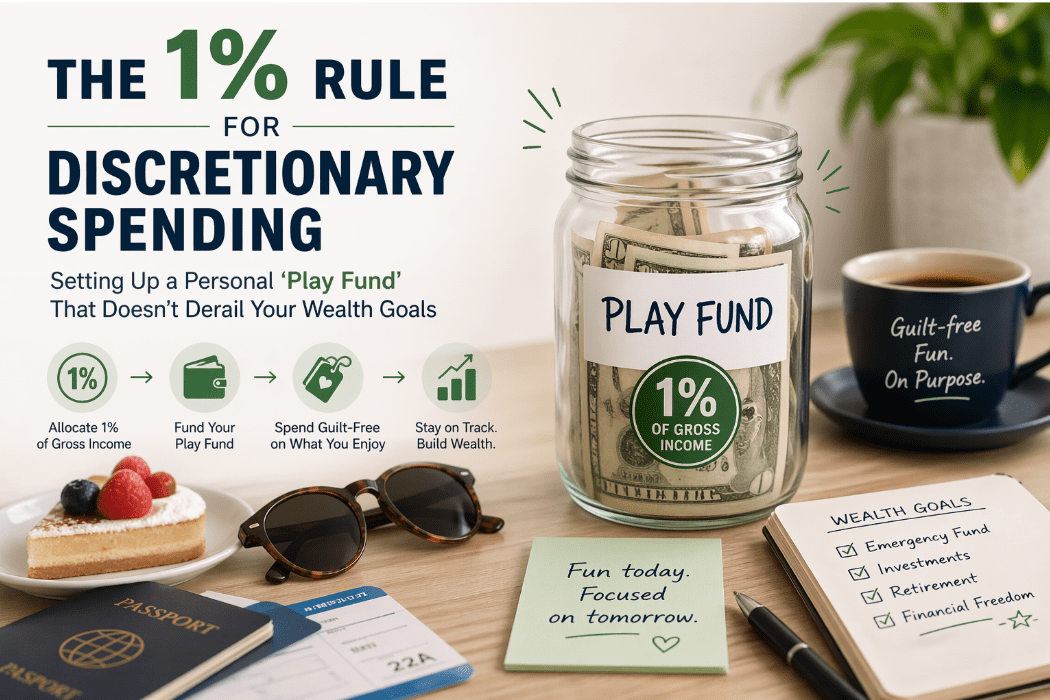

But here’s the reality: sustainable wealth-building isn’t about eliminating pleasure. It’s about containing it. And one of the most effective tools for doing that is what financial planners and behaviorally savvy investors increasingly call the 1% Rule for discretionary spending – the practice of deliberately allocating a fixed, small percentage of your net income or investable assets to a dedicated “Play Fund.”

Done correctly, this approach protects your long-term financial plan while giving you guilt-free permission to enjoy the money you’ve worked hard to earn.

What Is the 1% Rule, and Where Did It Come From?

The 1% Rule in discretionary spending borrows from a broader principle used across finance and real estate: defining a bounded, pre-approved budget that operates independently of your core wealth-building activities. Just as many real estate investors use a 1% rule to screen rental properties, the discretionary version applies a similar ceiling to entertainment and lifestyle spending.

In practice, it works like this: take 1% of your monthly after-tax income – or, for high-net-worth individuals, 1% of your monthly investable asset returns – and ring-fence it as untouchable fun money. This isn’t your emergency fund. It isn’t your travel budget or your vacation home maintenance line. It’s purely discretionary: the money you spend without needing to justify it to anyone, including yourself.

The number can be adjusted. Some practitioners prefer 0.5% for aggressive savers; others go up to 2% once their wealth targets are secured. But the principle is the same – containment through pre-commitment. You decide the size of the sandbox before you start playing in it, which means you’re never dipping into retirement accounts or investment capital to fund a night out.

Why a Dedicated Play Fund Actually Protects Your Wealth

The behavioral case for a Play Fund is as strong as the financial one. Research in consumer psychology consistently shows that people who attempt to eliminate all discretionary spending entirely tend to experience what’s called “restraint collapse” – a sudden, poorly planned splurge that far exceeds what moderate, regular enjoyment would have cost them.

Think of it as the financial equivalent of crash dieting. Rigid restriction leads to bingeing. Structured moderation leads to consistency.

A Play Fund creates a psychological permission structure. When you’ve pre-allocated $400 (or $2,000, or $10,000 – the absolute number depends on your income) to leisure each month, you no longer need to negotiate with yourself every time you want to spend it. The decision has already been made. The budget is set. You simply spend within it and move on.

This is particularly important for high earners and investors whose wealth management strategy is already sophisticated. When your financial architecture is carefully designed – diversified portfolio, structured cash flow, risk-adjusted returns – the last thing you want is behavioral leakage: small, unplanned emotional purchases that accumulate into something meaningful over time.

What Goes in the Play Fund?

The short answer: anything that’s purely for enjoyment and doesn’t produce a financial return. Dinners, concerts, hobby gear, sporting events, wellness experiences, and digital entertainment all qualify. So does online gaming.

This is worth addressing directly, because the iGaming space has seen a significant shift in how financially literate players engage with it. The rise of frictionless payment systems – particularly pay n play casinos – has made it easier than ever to deposit, play, and withdraw with a few clicks and no lengthy registration process. For someone operating with a Play Fund, this is actually a feature, not a risk. When your budget is pre-set and your payment is handled through a verified banking infrastructure like a trustly casino, the transaction is transparent, traceable, and bounded. You know exactly how much you’ve spent, and you can reconcile it against your Play Fund in real time.

The key, as with any discretionary category, is that gaming activity draws from the Play Fund – not from savings, not from investment capital, and certainly not from emergency reserves. Used this way, it becomes just another line item in a well-managed personal budget, no different from a spa membership or a season ticket package.

Setting Up Your Play Fund: A Practical Framework

Step 1: Calculate your baseline. Start with your monthly after-tax income. If you’re drawing from investment returns, use the realized returns in a given month. Apply your chosen percentage – 1% is a sensible starting point – and that number becomes your Play Fund ceiling.

Step 2: Open a separate account or designate a separate card. Behavioral finance research shows that mental accounting works better when it’s physical. Having a distinct account or prepaid card for discretionary spending makes overspending immediately visible. When the balance hits zero, the month’s fun budget is done – full stop.

Step 3: Automate the transfer. On the same day your income arrives, move the Play Fund allocation automatically. This mirrors the “pay yourself first” principle used in investing. You’re not spending what’s left after savings – you’re allocating what you’ve pre-approved for leisure before the rest of your budget even engages.

Step 4: Track, but don’t obsess. A monthly review of what you spent the Play Fund on is useful – not to induce guilt, but to see whether your choices actually brought you satisfaction. Did that extra dinner out feel as rewarding as a gaming session you’d been looking forward to all week? Did a last-minute impulse buy feel hollow afterward? This kind of light reflection sharpens your discretionary preferences over time and helps you get more genuine enjoyment per dollar.

Step 5: Respect the ceiling – especially during volatile periods. When markets are down or you’re navigating a period of financial uncertainty, the Play Fund should not expand to compensate emotionally. If anything, it’s a floor – the minimum commitment to your own wellbeing – not a place to seek financial relief. Solid wealth protection strategies are built on emotional discipline as much as financial mechanics.

The Bigger Picture: Wealth Isn’t Just a Number

There’s a version of financial discipline that becomes its own trap – where every dollar is so aggressively optimized that life itself starts to feel like a spreadsheet. The 1% Play Fund is a deliberate counterweight to that tendency.

Wealthy individuals who sustain their financial health over decades aren’t people who never spend on fun. They’re people who spend on fun strategically – knowing exactly what they’ve committed, why they’ve committed it, and how it fits into the larger picture of a life well-lived.

A well-designed Play Fund acknowledges that you are not a portfolio. You are a person. And part of managing wealth intelligently is managing the human experience that wealth is ultimately supposed to support.

Set the fund. Respect the ceiling. Enjoy what’s inside it – fully, without apology.