A good credit score can open the door to better financial opportunities, including lower interest rates, easier loan approvals, higher credit card limits, and even better insurance premiums. If your score isn’t where you’d like it to be, the good news is that there are legal and effective ways to improve it quickly.

Whether you’re planning to apply for a mortgage, auto loan, personal loan, or credit card, understanding how to improve your credit score fast and legally can save you thousands of dollars over time. While there are no overnight miracles, following the right strategies can help you see noticeable improvements within a few months.

In this guide, you’ll learn proven methods to boost your credit score while avoiding scams and risky shortcuts.

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness. Lenders use it to determine how likely you are to repay borrowed money. Most credit scores range from 300 to 850, with higher scores indicating lower financial risk.

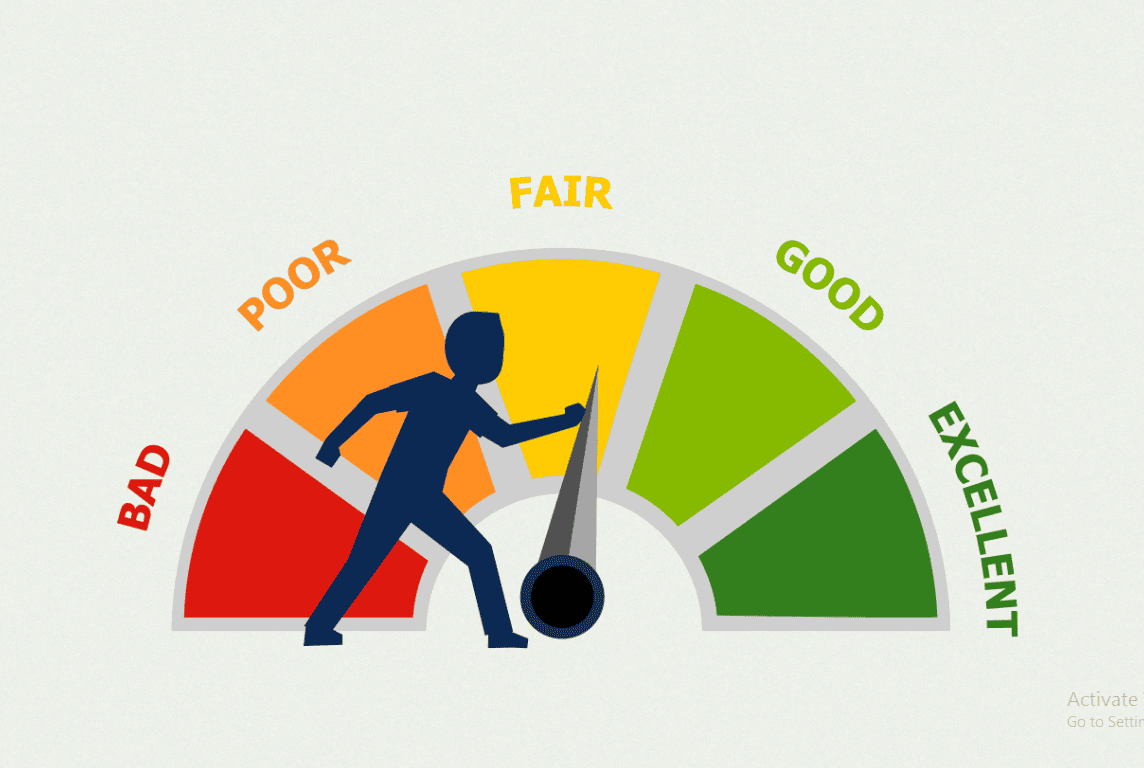

Generally, credit score ranges are:

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–850: Excellent

Improving your score can help you qualify for better financial products and lower borrowing costs.

Why Your Credit Score Matters

Your credit score affects more than just loan approvals. A higher score can provide several financial benefits, including:

- Lower interest rates on loans

- Better credit card offers

- Higher credit limits

- Easier approval for mortgages

- Improved chances of renting an apartment

- Better financing options for vehicles

- Lower security deposits for utilities

Even a small increase in your score can make a significant difference over the life of a loan.

Ways to Improve Your Credit Score Fast and Legally

1. Pay Your Bills on Time

Payment history is one of the most important factors affecting your credit score. Even a single missed payment can negatively impact your credit.

To stay on track:

- Set up automatic payments.

- Use payment reminders.

- Pay at least the minimum amount due each month.

- Never ignore overdue accounts.

Consistent on-time payments build trust with lenders and gradually improve your credit profile.

2. Reduce Your Credit Utilization

Credit utilization refers to the percentage of your available credit that you’re currently using.

For example, if your credit card limit is $10,000 and your balance is $2,000, your utilization rate is 20%.

Experts generally recommend keeping utilization below 30%, while staying below 10% can produce even better results.

Ways to lower utilization include:

- Paying off credit card balances early.

- Making multiple payments during the month.

- Requesting a credit limit increase without increasing spending.

Lower utilization signals responsible credit management.

3. Review Your Credit Report for Errors

Mistakes on your credit report can lower your score unfairly.

Check your report carefully for:

- Incorrect late payments

- Accounts you don’t recognize

- Duplicate debts

- Incorrect balances

- Personal information errors

If you find inaccuracies, dispute them with the credit bureau. Correcting errors can sometimes result in a noticeable score increase.

4. Avoid Applying for Too Many New Credit Accounts

Each new credit application may result in a hard inquiry, which can temporarily lower your credit score.

Instead of applying for several credit cards or loans at once:

- Only apply when necessary.

- Compare offers before submitting applications.

- Space out credit applications over time.

Fewer hard inquiries help maintain a stronger credit profile.

5. Keep Older Credit Accounts Open

The length of your credit history contributes to your overall score.

Closing old credit cards can:

- Reduce your average account age.

- Increase your credit utilization.

- Lower your available credit.

If an older account has no annual fee, consider keeping it open and using it occasionally for small purchases.

6. Pay Down Existing Debt

Reducing outstanding debt is one of the fastest ways to improve your credit score.

Focus on:

- Credit card balances

- Personal loans

- Lines of credit

Many people use one of these repayment strategies:

Debt Avalanche Method

Pay extra toward the debt with the highest interest rate while making minimum payments on the others.

Debt Snowball Method

Pay off the smallest balance first to build momentum before moving to larger debts.

Both methods help improve your financial health over time.

7. Become an Authorized User

If a trusted family member has a long history of responsible credit use, becoming an authorized user on their credit card may help improve your credit profile.

This strategy works best when the primary cardholder:

- Pays bills on time

- Maintains low balances

- Has a long credit history

However, ensure the card issuer reports authorized user activity to the credit bureaus.

8. Avoid Closing Paid-Off Credit Cards

Many people close credit cards after paying them off, but doing so can reduce your available credit and increase your utilization ratio.

Keeping older cards open—especially those with no annual fee—can support a healthier credit score.

9. Negotiate Outstanding Collections

If you have accounts in collections, paying or settling them may improve your overall credit profile.

Before making payment:

- Confirm the debt is accurate.

- Request written documentation.

- Ask whether the creditor will update the account after payment.

Although paid collections may remain on your report for some time, resolving outstanding debts demonstrates financial responsibility.

10. Monitor Your Credit Regularly

Regular credit monitoring helps you:

- Detect fraud early

- Track score improvements

- Identify reporting errors

- Stay informed about changes

Monitoring your credit also helps you understand how your financial decisions affect your score.

Common Mistakes That Hurt Your Credit Score

Avoid these common credit mistakes:

- Missing payment due dates

- Maxing out credit cards

- Closing old accounts unnecessarily

- Applying for multiple loans within a short period

- Ignoring collection notices

- Co-signing loans without understanding the risks

Good financial habits are often more effective than quick fixes.

How Long Does It Take to Improve a Credit Score?

The timeline depends on your current credit profile and the actions you take.

- Paying down credit card balances may improve your score within one or two billing cycles.

- Correcting credit report errors can lead to improvements once the updates are processed.

- Building a strong payment history usually takes several months.

- Recovering from serious negative events, such as defaults or bankruptcies, may take years.

Patience and consistency are essential for long-term success.

Can Credit Repair Companies Help?

Some credit repair companies offer legitimate services, such as reviewing credit reports and disputing inaccuracies on your behalf. However, they cannot remove accurate negative information or guarantee a higher score.

Many of the steps they perform—like reviewing your report and disputing errors—can be done on your own at little or no cost. Be cautious of companies that promise instant results or ask for large upfront fees.

Final Thoughts

Improving your credit score fast and legally requires a combination of smart financial habits and consistent effort. Paying bills on time, reducing credit card balances, checking your credit reports for errors, limiting new credit applications, and keeping older accounts open are among the most effective ways to boost your score.

While significant improvements may take time, even small positive changes can increase your borrowing power and help you qualify for better interest rates. By following these proven strategies, you’ll build stronger credit and improve your overall financial health.

Frequently Asked Questions (FAQs)

1. What is the fastest legal way to improve a credit score?

Paying down high credit card balances, making all payments on time, and correcting errors on your credit report are among the fastest legal ways to improve your credit score.

2. How much can my credit score improve in 30 days?

The increase varies depending on your financial situation. Some people may see improvements after lowering credit utilization or correcting reporting errors, while others may need more time.

3. Does paying off a credit card improve my credit score?

Yes. Paying off or significantly reducing your credit card balance lowers your credit utilization, which can positively impact your score.

4. Should I close a credit card after paying it off?

Not necessarily. Keeping older credit cards open, especially those without annual fees, can help maintain a longer credit history and lower your credit utilization ratio.

5. Can checking my own credit score lower it?

No. Checking your own credit score is considered a soft inquiry and does not affect your credit score.

6. How often should I review my credit report?

It’s a good idea to review your credit report at least once a year, or more frequently if you’re planning to apply for credit or want to monitor your financial progress.

7. Can late payments be removed from my credit report?

Accurate late payments generally remain on your credit report for several years. However, incorrect late payment records can be disputed and removed if verified as errors.

8. Is hiring a credit repair company worth it?

It depends on your situation. While some companies provide legitimate assistance, many tasks they perform can be completed independently. Always research a company’s reputation before signing up for its services.