Creating a financial plan for the next five years is essential for achieving long-term goals, building wealth, and ensuring financial stability. Whether you aim to buy a house, start a business, save for retirement, or pay off debt, a clear and actionable financial plan provides direction and accountability.

This guide walks you through step-by-step strategies to create a realistic five-year financial plan, manage income, control expenses, and optimize savings and investments.

Why a 5-Year Financial Plan Matters

A five-year financial plan allows you to balance short-term needs with long-term goals. Unlike a one-year budget, it focuses on sustained progress, helps anticipate financial challenges, and provides a roadmap for achieving significant milestones.

Benefits of a 5-Year Financial Plan:

-

Clarifies financial priorities

-

Encourages disciplined saving and spending

-

Prepares for emergencies and unexpected expenses

-

Helps track progress toward major goals

-

Reduces financial stress and uncertainty

Steps to Create a 5-Year Financial Plan

| Step | Action | Purpose |

|---|---|---|

| 1 | Define Your Financial Goals | Identify short-term (1 year) and long-term (5 years) objectives |

| 2 | Assess Current Financial Situation | List income, expenses, assets, and liabilities |

| 3 | Create a Budget | Track monthly cash flow and allocate for goals |

| 4 | Build an Emergency Fund | Save 3–6 months of essential expenses |

| 5 | Manage Debt Strategically | Pay off high-interest debt first |

| 6 | Plan Savings & Investments | Allocate funds to retirement, stocks, or other investment options |

| 7 | Monitor & Adjust Regularly | Review progress quarterly or annually |

| 8 | Consider Insurance & Protection | Health, life, and disability insurance |

1. Define Your Financial Goals

Start by listing what you want to achieve in the next five years. Goals should be specific, measurable, achievable, relevant, and time-bound (SMART). Examples include:

-

Saving for a home down payment

-

Paying off student loans

-

Building an emergency fund

-

Investing for retirement or education

2. Assess Current Financial Situation

Evaluate your current income, expenses, assets, and liabilities. Knowing your baseline helps determine how much you can save and invest toward your five-year goals. Consider using personal finance software or spreadsheets for accuracy.

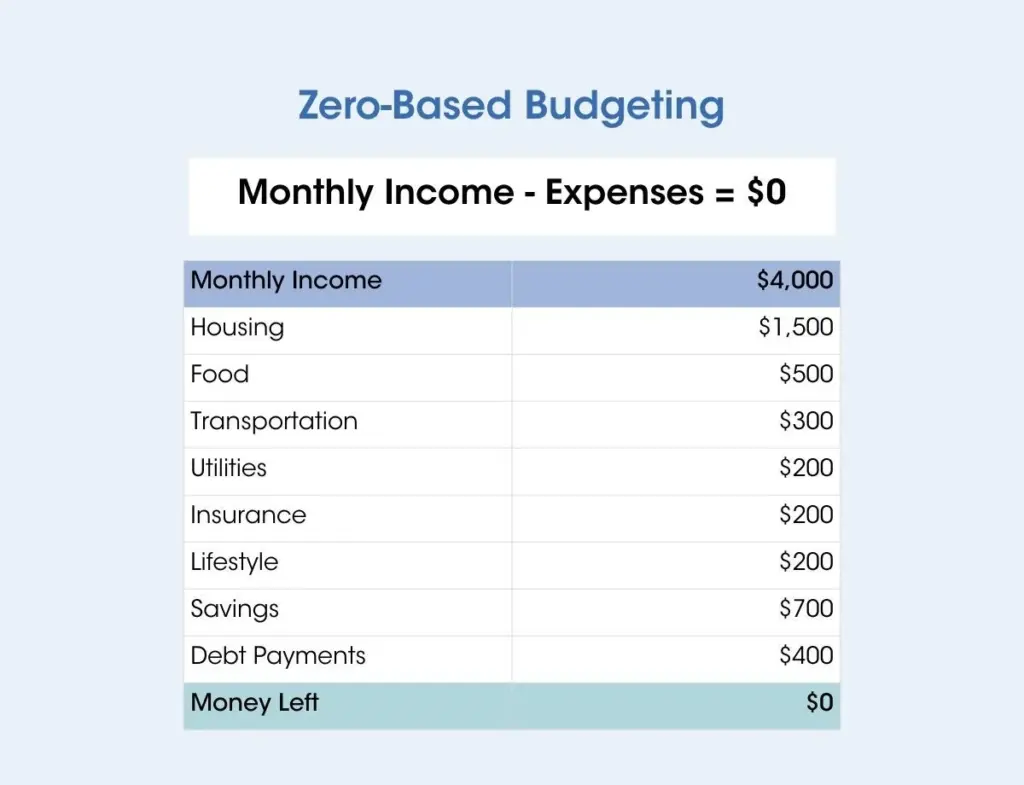

3. Create a Budget

A budget allocates your income toward essentials, discretionary spending, debt repayment, and savings. A clear monthly budget helps identify areas to cut back and increases contributions toward your long-term goals.

4. Build an Emergency Fund

Unexpected expenses, such as medical bills or car repairs, can derail your financial plan. Saving 3–6 months’ worth of essential expenses in a liquid, easily accessible account provides a financial safety net.

5. Manage Debt Strategically

High-interest debts, such as credit cards or personal loans, can hinder financial progress. Prioritize paying off high-interest debt first while maintaining minimum payments on other obligations. Consider debt consolidation or refinancing if it reduces interest rates.

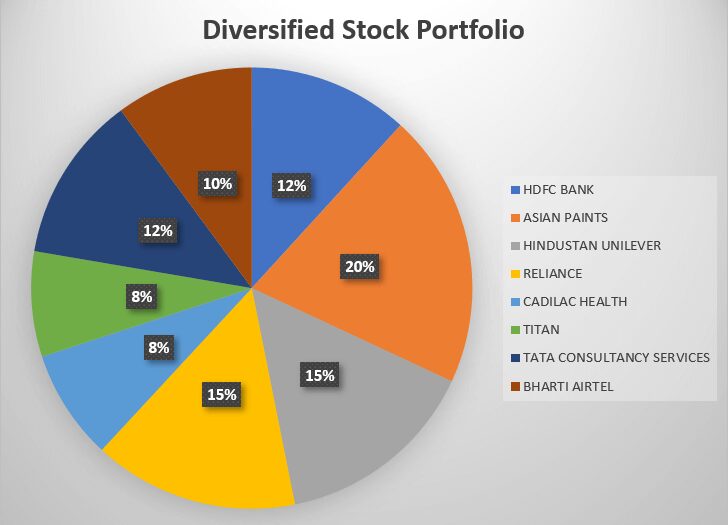

6. Plan Savings and Investments

Allocating funds to savings and investments is critical for long-term growth. Options include:

-

Retirement accounts: 401(k), IRA, or pension plans

-

Stocks and mutual funds: For long-term wealth accumulation

-

High-yield savings accounts or bonds: For medium-term goals

-

Automatic contributions: Ensures consistent growth

7. Monitor and Adjust Regularly

Life circumstances, income, and expenses can change. Review your financial plan at least quarterly to ensure you’re on track and adjust goals, contributions, or spending as needed.

8. Consider Insurance and Protection

Adequate insurance coverage protects your assets and income. Health, life, disability, and property insurance reduce the risk of financial setbacks, ensuring your five-year plan stays on track.

Tips for a Successful 5-Year Financial Plan

-

Be realistic: Set achievable goals based on income and lifestyle

-

Prioritize: Focus on high-impact goals first

-

Automate savings: Use automatic transfers to stay consistent

-

Track progress: Use apps, spreadsheets, or financial advisors

-

Stay disciplined: Avoid unnecessary expenses that derail your plan

Common Mistakes to Avoid

-

Ignoring inflation and changing costs

-

Overestimating income or underestimating expenses

-

Failing to adjust for life changes (job change, family growth)

-

Neglecting debt repayment while saving aggressively

-

Not reviewing progress regularly

FAQs

Q1: How much should I save each year for a 5-year plan?

Aim to save at least 20% of your income, adjusting based on debt obligations, goals, and lifestyle needs.

Q2: Should investments be included in a 5-year plan?

Yes. Investments help grow wealth over time using compound interest, but consider risk tolerance and liquidity needs.

Q3: Can I achieve multiple goals simultaneously?

Yes. Allocate priorities and budget accordingly, balancing short-term needs and long-term objectives.

Q4: How do I handle unexpected financial emergencies?

Maintain an emergency fund separate from your savings for planned goals to avoid disruptions.

Q5: Do I need a financial advisor?

While optional, a financial advisor can provide guidance, help with investment strategy, and ensure your plan is realistic and tax-efficient.

Conclusion

Creating a financial plan for the next five years is an essential step toward achieving financial stability and reaching your life goals. By defining SMART goals, assessing your current financial situation, budgeting wisely, managing debt, and investing strategically, you can make meaningful progress. Regular monitoring and adjustments ensure that your plan remains aligned with life changes, providing a clear roadmap for financial success over the next five years.

With discipline, realistic expectations, and proactive planning, a well-structured five-year financial plan can transform your finances and set the foundation for long-term wealth.