Managing finances when your income fluctuates can be challenging. Freelancers, gig workers, entrepreneurs, and commission-based professionals often face months with high earnings followed by lean periods. Without a structured approach, it’s easy to overspend during peak months and struggle during slower ones.

Fortunately, there are budgeting methods designed specifically for people with variable income. These strategies help stabilize cash flow, prioritize expenses, and plan for both short-term needs and long-term financial goals.

Why Budgeting Matters for Variable Income

A consistent budget provides clarity and control over unpredictable earnings. Even if income varies, the right budgeting strategy ensures that essential expenses are covered, debt is managed, and savings continue to grow.

Benefits of Budgeting with Variable Income

-

Smooth out months with fluctuating earnings

-

Avoid overspending during high-income months

-

Maintain an emergency fund for low-income periods

-

Stay on track toward financial goals

-

Reduce financial stress and uncertainty

Top Budgeting Methods for Variable Income

| Method | How It Works | Best For |

|---|---|---|

| Zero-Based Budgeting | Assign every dollar a purpose, including savings and debt | Ensures all income is allocated efficiently |

| Percentage-Based Budgeting | Allocate income by fixed percentages (e.g., 50% essentials, 30% savings, 20% discretionary) | Flexible for fluctuating earnings |

| Baseline Budgeting | Cover only essential expenses first, then allocate surplus to savings or discretionary spending | Provides security during lean months |

| Rolling Average Budgeting | Calculate average income over 6–12 months to plan monthly spending | Smooths out fluctuations and stabilizes budget |

| Priority-Based Budgeting | Prioritize expenses from most essential to least | Ideal for freelancers or seasonal workers |

| Envelope System | Divide cash into envelopes for specific categories | Helps control spending and stick to a plan |

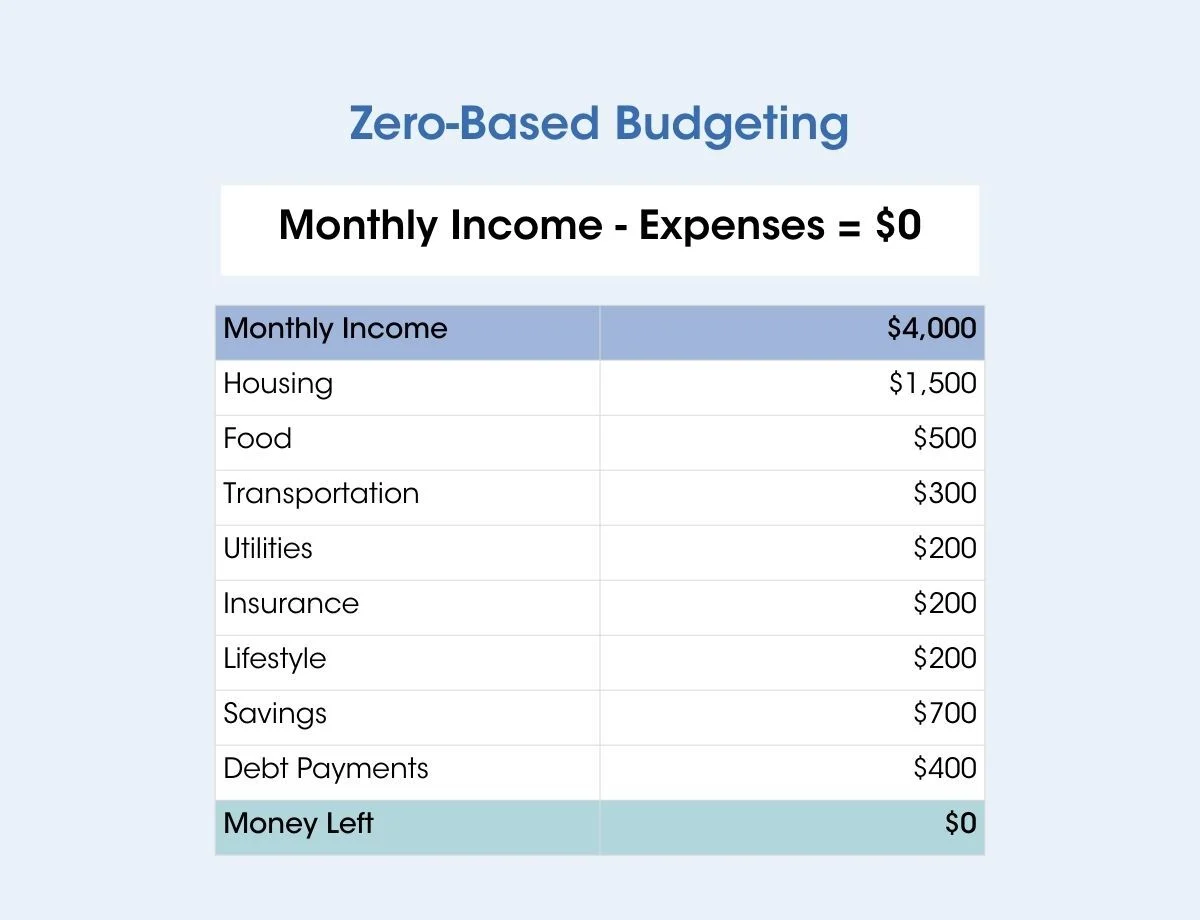

1. Zero-Based Budgeting

Zero-based budgeting assigns every dollar of income to a specific category, including savings and debt repayment. For variable income, start with your essential expenses first, then allocate surplus funds to financial goals. This method ensures no money is wasted and helps track spending carefully.

2. Percentage-Based Budgeting

This method allocates a percentage of your income to various categories, such as essentials, savings, and discretionary spending. For example:

-

50% for essentials (rent, utilities, groceries)

-

30% for savings or debt repayment

-

20% for lifestyle and discretionary spending

Percentages adjust naturally with variable income, keeping your budget flexible yet structured.

3. Baseline Budgeting

Baseline budgeting focuses on covering only the essentials first. Once your fixed costs are met, surplus income can be directed toward savings, investment, or fun activities. This method protects you during months when earnings are low, ensuring critical expenses are always covered.

4. Rolling Average Budgeting

Rolling average budgeting calculates your average monthly income over a period (usually 6–12 months) to establish a stable spending plan. This helps normalize fluctuating earnings and prevents overspending in high-income months.

5. Priority-Based Budgeting

In priority-based budgeting, expenses are ranked by importance. Essentials like rent, utilities, and debt payments are addressed first. Remaining funds go to secondary needs and discretionary spending. This approach provides a safety net for unpredictable income streams.

6. Envelope System

The envelope system uses physical or digital “envelopes” to allocate money for specific categories, such as groceries, transportation, or entertainment. Spending is limited to the amount in each envelope, helping control overspending and forcing financial discipline.

Tips for Budgeting with Variable Income

-

Track income carefully: Document all income sources and dates.

-

Build a buffer: Save during high-income months to cover lean periods.

-

Separate fixed and flexible expenses: Know which costs must be paid and which can be adjusted.

-

Automate savings: Set up automatic transfers for emergencies and long-term goals.

-

Review monthly: Adjust budget allocations as income changes.

-

Focus on essentials first: Always prioritize rent, utilities, debt, and groceries.

Common Mistakes to Avoid

-

Spending based on projected or “best-case” income

-

Neglecting to save during high-income months

-

Ignoring irregular bills or annual expenses

-

Mixing business and personal finances if freelancing

-

Not reviewing and adjusting the budget regularly

FAQs

Q1: Can a variable income budget be the same every month?

No. Your budget must be flexible to account for fluctuations. Using averages or percentages helps maintain consistency while adjusting for changes in income.

Q2: How much should I save during high-income months?

Aim to save 20–50% of surplus income, depending on your essential expenses and financial goals.

Q3: Which method is best for freelancers?

Baseline budgeting or priority-based budgeting works well, ensuring essential expenses are always covered and surplus income is allocated wisely.

Q4: How do I handle irregular or seasonal income?

Track earnings over time and build a rolling average budget. This smooths out highs and lows and prevents financial stress during lean months.

Q5: Can I combine budgeting methods?

Yes. Many people combine approaches, such as using a baseline budget for essentials and the envelope system for discretionary spending.

Conclusion

Budgeting with variable income requires flexibility, planning, and discipline. Methods like zero-based budgeting, percentage-based budgeting, and rolling average budgeting provide structure while accommodating fluctuating earnings. Prioritizing essentials, building savings during high-income months, and regularly reviewing your finances ensures stability and progress toward long-term financial goals.

By adopting a method that fits your income pattern and lifestyle, you can reduce financial stress, maintain control over spending, and create a sustainable plan that works throughout the year, regardless of income variability.