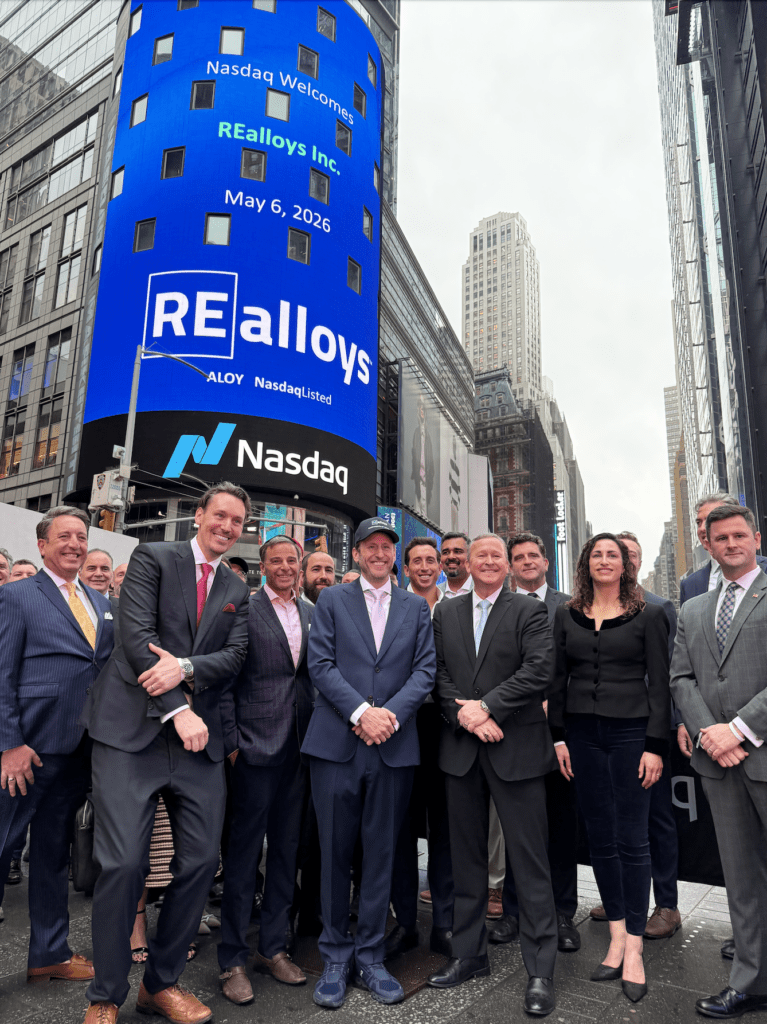

When REalloys rang the Nasdaq Closing Bell on May 6, 2026 in Times Square, the ceremony marked more than a public-market milestone for a newly listed company. It came at a moment when Washington, defense contractors and critical-minerals investors are increasingly focused on one of the weakest links in the U.S. industrial base: the ability to turn rare earth oxides into metals used in magnets for weapons, electronics and advanced manufacturing.

REalloys, which trades on Nasdaq under the ticker ALOY, began trading after its merger with Blackboxstocks in February. Days later, the Ohio-based rare earths company announced it had been awarded a U.S. Department of Defense contract intended to fund design work for a processing facility that would convert heavy rare earths into metal form. The award covers a two-phase, 24-month effort to develop engineering schematics for a modular processing facility. REalloys is targeting capacity of up to 300 metric tons a year of samarium and gadolinium metals, materials used in magnets for defense systems, electronics and other high-performance applications. Rare earths must be converted into metals before they can be made into magnets, a step that is extremely limited in the U.S. supply chain and non existent at a large scale. The scale needed to gain independence from China.

The Nasdaq bell-ringing gave REalloys a public stage as rare earths move further into the center of U.S.-China trade and national-security policy. On Sunday, the White House said China had agreed to address U.S. concerns over shortages of critical minerals including yttrium, scandium, indium and neodymium, following recent leader-level talks. But the statement stopped short of saying Beijing would remove its export controls, which Reuters reported have disrupted U.S. aerospace and semiconductor manufacturing.

The vulnerability has become more visible as geopolitical tensions rise. China’s restrictions, introduced in April 2025, remain in place, underscoring the leverage Beijing holds over materials used in aircraft engines, next-generation chips, electronics, electric vehicles and defense systems. For Washington, the issue is no longer simply whether minerals can be mined, but whether the U.S. and its allies can build the downstream capacity to separate, refine and convert them into usable industrial inputs.

That is the gap REalloys is seeking to address.

The company is developing a rare earths mine in Saskatchewan and has a processing agreement with the Saskatchewan Research Council, the Canadian province’s technology innovation unit. It is also building out metallization capabilities in Euclid, Ohio, where rare earth oxides can be converted into metals and magnet-grade alloys.

The company has said its approach is aimed at creating a North American chain that runs from feedstock to separated oxides to metals and, eventually, magnet-grade products. That strategy reflects a larger shift in the critical-minerals sector. Mining assets alone are no longer enough. The bottleneck is increasingly in the industrial middle of the supply chain, where raw or semi-processed materials are converted into forms manufacturers can use.

Heavy rare earths are especially sensitive. Elements such as dysprosium and terbium help magnets retain performance at high temperatures, making them important for defense systems, aerospace, robotics and electric mobility. Samarium and gadolinium, the focus of the Defense Logistics Agency contract, are used in specialized magnet and defense-related applications.

REalloys meanwhile has moved to secure additional feedstock. The company recently signed a memorandum of understanding with U.S. Critical Materials Corp. for access to up to 10% of production from the Sheep Creek project in Montana, which contains dysprosium, terbium, yttrium and NdPr, rare earth elements used in high-performance magnets for fighter aircraft, missile guidance systems and radar platforms.

The timing matters.

Beginning in January 2027, certain U.S. defense rules are expected to restrict the use of Chinese-origin rare earth materials in American military systems, creating pressure on contractors and suppliers to qualify alternative sources. REalloys’ strategy is built around that deadline, though building new metallization capacity remains a difficult and capital-intensive task.

“Metallization is one of the least developed parts of the value chain outside China,” REalloys co-founder Tim Johnston has said. “Even with strong execution and capital, you are looking at a multi-year timeline to build that capability.”

The company’s advisory bench also reflects the defense orientation of the business. REalloys recently added Joe Kasper, former chief of staff to the U.S. Secretary of Defense, to its advisory board. He joins figures including retired Gen. Jack Keane, former vice chief of staff of the U.S. Army, and Stephen duMont, president of GM Defense.

For investors, the company sits inside a theme that has gained new urgency: the rebuilding of domestic and allied industrial capacity in sectors once treated as globalized commodities. The Biden and Trump administrations both pushed to secure critical minerals, and defense agencies have increasingly used contracts, financing tools and procurement policy to encourage the development of non-Chinese supply chains.

REalloys is an early-stage public company operating in a technically demanding market with a leadership team that demonstrates where they are going . Scaling metallization and magnet production will require execution, capital and customer qualification. The company’s Nasdaq appearance underscores how rare earths have become part of a larger capital-markets conversation around supply-chain resilience, defense readiness and industrial sovereignty.