In the realm of real estate, the landscape is shifting as homeowners navigate the fluctuating terrain of mortgage rates. Last year witnessed a significant dip in existing home sales, marking a nadir not seen in almost three decades. The culprit? A phenomenon dubbed the “lock-in effect” – a scenario where homeowners, benefiting from below-market mortgage rates, are hesitant to sell amidst higher rate climates.

Imagine being ensconced in a mortgage at a 3% rate; the notion of relinquishing such favorable terms, particularly in exchange for an 8% rate, seems untenable. While mortgage rates have tapered slightly, hovering at an average of 7.11% for a 30-year fixed rate, it remains considerably higher than the historic lows experienced during the pandemic and preceding years.

Recent analysis from Zillow’s senior economist, Orphe Divounguy, casts doubt on the easing of the lock-in effect. Despite a notable 21% uptick in new listings in February compared to the same period last year, Divounguy highlights that this surge primarily occurred in markets boasting a substantial cohort of homeowners unburdened by mortgage rate lock-ins.

Metropolitan areas with a prevalence of mortgage-free homeowners witnessed the most pronounced increase in listings, indicating a segment of the populace deemed “mortgage-ready” by Zillow. These individuals, numbering almost 11 million, possess the financial bandwidth to navigate the real estate landscape, regardless of prevailing mortgage rates.

Primarily comprising older generations, including baby boomers and their silent predecessors, these homeowners have accrued substantial home equity over the years. Consequently, they can comfortably entertain the prospect of acquiring another property, even amidst a 7% mortgage rate environment.

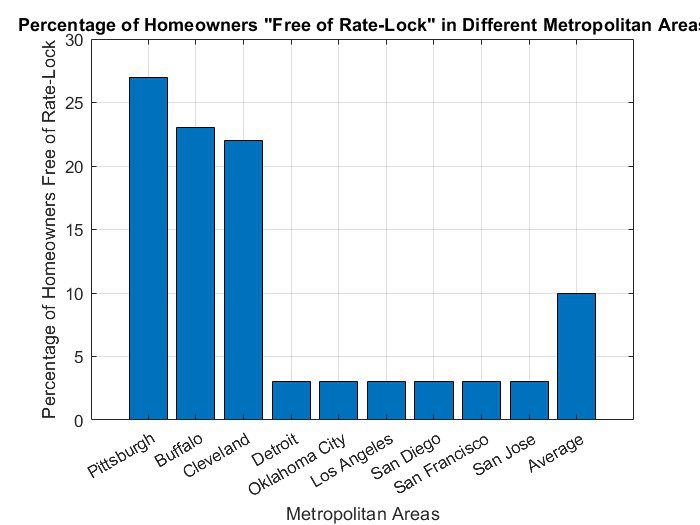

Conversely, millennials find themselves disproportionately impacted by the lock-in effect, with only 6% of millennial homeowners shielded from its constraints. Metropolitan areas such as Detroit, Cleveland, Oklahoma City, Buffalo, and Pittsburgh emerge as bastions where homeowners are less susceptible to rate fluctuations, contrasting starkly with California cities like Los Angeles, San Diego, San Francisco, and San Jose, where only 3% of homeowners enjoy a similar reprieve.

The lock-in effect’s ramifications reverberate across the housing market, contributing to supply constraints and price escalation. Research indicates that the lock-in effect led to a staggering reduction in home sales, resulting in a 5.7% uptick in home prices amidst challenging affordability conditions.

Despite these challenges, signs of a thaw in supply dynamics are emerging, with existing home sales witnessing a notable surge in February, marking the most substantial monthly increase in a year. However, the narrative of this year’s spring shopping and selling season might resemble a scaled-down version of the norm, given the persistent high mortgage rates, soaring home prices, stagnant incomes, and a shortfall of millions of homes.

As the real estate landscape continues to evolve, homeowners and market observers alike remain poised to navigate the nuanced interplay between mortgage rates, supply dynamics, and buyer sentiment. Stay tuned as ImpactWealth.Org continues to unravel insights into the ever-shifting domain of real estate and wealth management.