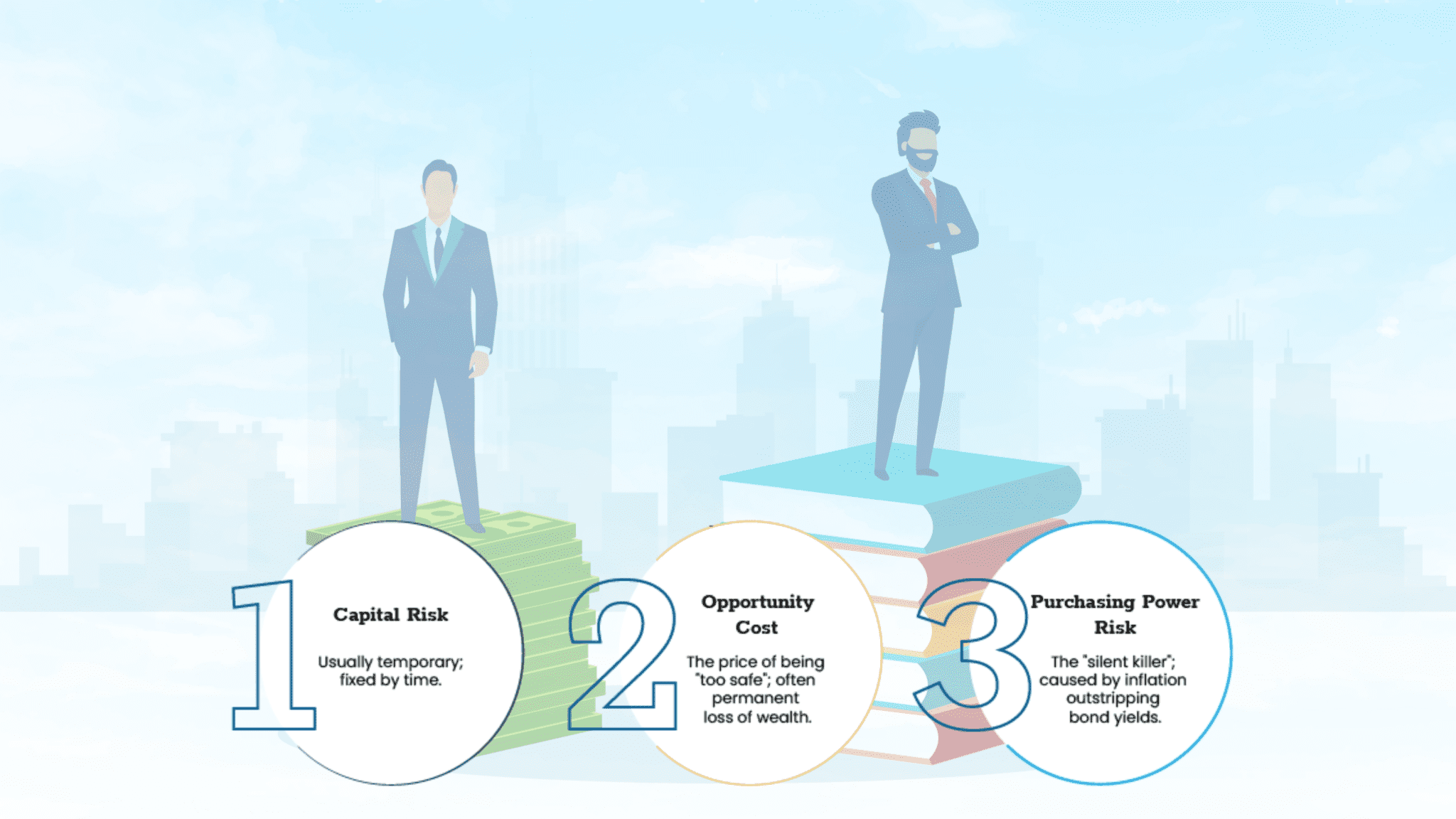

Investors should be aware of all investment risks when investing, but they are not. The one risk that seemingly gets 99% of attention from investors is risk to capital. Investors typically fret over volatility by equating high volatility with high risk. What they fail to recognize is that the most volatile assets lead to the highest returns over time.

Clearly, stocks are regarded as being more volatile than bonds. However, risks associated with investing in the stock market dissipate over time. There have been three instances since WW II whereby stocks have lost 48% or more in bear markets. In every instance, the stock market has fully recouped these losses en route to going on and establishing new record highs.

It’s essential to adopt a long-term time horizon when investing in the stock market to minimize capital risk. Rolling 10-year returns for the S&P 500 through 2024 show a 221% cumulative return on average since 1971. Over 20-year periods, the average cumulative return jumps to 880%. Cumulative returns in both periods have far outpaced the corresponding rise in inflation as measured by the CPI, which has led to big gains in purchasing power.

Risk number two relates to lost opportunity costs. Looking at HFRI hedge fund data tells quite a story. Over 10 years ending 2024, the typical long bias equities hedge fund earned a cumulative return of 84% versus 245% for the S&P 500. Hence, the lost opportunity costs by not being fully invested in stocks were almost twice as great as money earned by long bias equities hedge funds.

Risk number three relates to loss of purchasing power, which is rarely considered by investors. Some major advisories have advocated maintaining a very heavy exposure in bonds throughout retirement. Specifically, these advisors key off the “the rule of 100” which is derived from subtracting one’s age from 100 to arrive at one’s equity exposure. In the case of a 65-year-old, the portfolio mix would be 65% in bonds and 35% in stocks according to this methodology. In some cases, unduly conservative investors will hold a portfolio of 100% invested in bonds.

How did a 100% investment in long government bonds fare over the past 10 years? NYU Stern Business School’s research shows that an investment in 10-year government bonds returned 2.7% on a cumulative basis for 10-years ending 2024.

Meanwhile, the Consumer Price Index advanced at a 32% clip over the same period, which led to a significant decline in purchasing power for this bond portfolio. In summary, investors need to consider possible loss of opportunity costs and possible loss in purchasing power in addition to capital risk in formulating their investment strategy. History shows that ignoring opportunity and purchasing power risks can turn into financial penalties down the road.

****

Robert Zuccaro, CFA is the Founder & Chief Investment Officer at Golden Eagle Strategies. Robert has over four decades of experience in equity research and fund management, having led institutional portfolios through multiple market cycles. He’s been recognized by national financial publications for his work in systematic investing.

Email:info@goldeneaglestrategies.com / phone: (561) 510-6606