Creating a financial plan from scratch can feel overwhelming, especially if you’re new to budgeting, investing, or managing long-term goals. However, a well-structured financial plan provides a roadmap for achieving financial stability, building wealth, and preparing for emergencies. By following a step-by-step approach, anyone can develop a comprehensive financial plan tailored to their needs and lifestyle.

This guide outlines practical steps to create a financial plan from scratch, covering budgeting, saving, investing, and risk management.

Step 1: Assess Your Current Financial Situation

Before making any plans, you need a clear understanding of where you stand financially.

Key Actions:

-

List all sources of income, including salary, freelance work, and side hustles.

-

Record monthly expenses, separating essentials (rent, utilities, groceries) from discretionary spending (entertainment, dining out).

-

Track debts, including credit cards, loans, and mortgages, along with interest rates.

-

Calculate net worth: assets minus liabilities.

Tip: Use financial apps or spreadsheets to monitor your cash flow and visualize your financial health.

Step 2: Set Clear Financial Goals

Goals give your financial plan purpose and direction. Categorize them by timeline:

-

Short-term goals: Pay off credit card debt, build a $1,000 emergency fund, save for a vacation.

-

Medium-term goals: Save for a home down payment, buy a car, or fund higher education.

-

Long-term goals: Retirement planning, investing for wealth growth, or funding children’s education.

Tip: Make your goals SMART—specific, measurable, achievable, relevant, and time-bound.

Step 3: Build an Emergency Fund

A solid emergency fund is the foundation of any financial plan. It protects you from unexpected expenses such as medical bills, home repairs, or sudden loss of income.

Actions:

-

Aim to save 3–6 months of living expenses.

-

Keep the fund in a separate, easily accessible account.

-

Contribute consistently, even if starting small.

Tip: Strategies similar to Emergency Fund Strategies for Single Parents work well for everyone, emphasizing small, consistent contributions and maintaining liquidity.

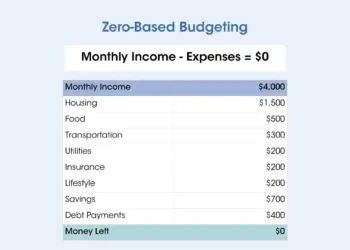

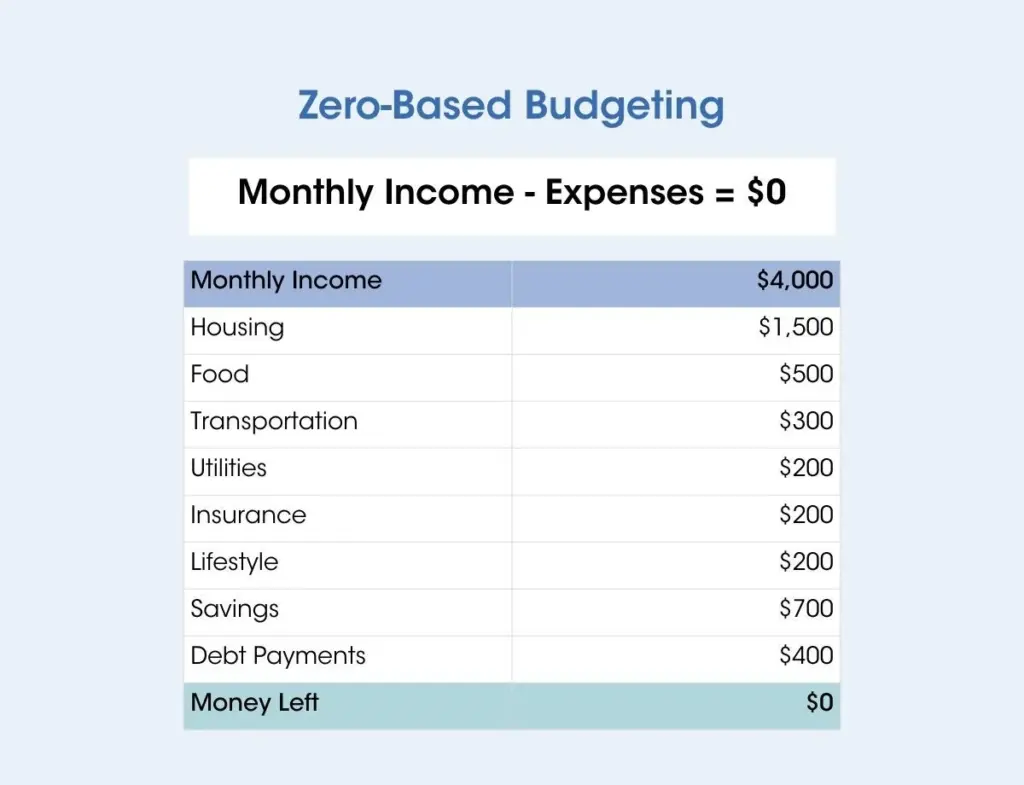

Step 4: Create a Budget

A budget helps control spending, ensures you’re saving enough, and aligns your finances with your goals.

Steps:

-

List all income and categorize monthly expenses.

-

Identify areas to reduce discretionary spending.

-

Allocate a percentage of income toward savings, debt repayment, and investments.

Tip: Follow the 50/30/20 rule as a guideline—50% for needs, 30% for wants, 20% for savings and debt repayment.

Step 5: Manage Debt Effectively

Debt can derail a financial plan if not managed properly. Prioritize paying off high-interest debt first.

Strategies:

-

Debt Avalanche: Pay off debts with the highest interest rates first.

-

Debt Snowball: Pay off the smallest balances first to build momentum.

-

Consolidate or refinance loans if it lowers interest rates.

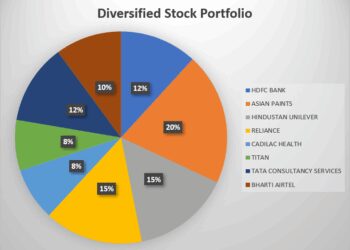

Step 6: Start Investing

Investing helps your money grow over time and ensures long-term financial security.

Options for beginners:

-

Retirement accounts: 401(k), IRA, or Roth IRA for tax-advantaged growth.

-

Stocks and ETFs: Start with index funds or ETFs for diversification.

-

Real estate or REITs: Consider options that align with small capital strategies.

Tip: Begin with what you can afford and gradually increase contributions as your income grows.

Step 7: Protect Yourself with Insurance

Risk management is an essential part of financial planning. Insurance safeguards against unforeseen events.

Essential coverage:

-

Health insurance

-

Life insurance if you have dependents

-

Disability insurance for income protection

-

Home or renter’s insurance to protect assets

Step 8: Monitor and Adjust Your Plan

A financial plan is not static. Life changes—such as career shifts, family growth, or economic conditions—require periodic adjustments.

Actions:

-

Review your plan quarterly or annually.

-

Reassess goals, savings rate, and investments.

-

Adjust spending and investment strategies based on progress.

Financial Plan Summary Table

| Step | Action | Benefit |

|---|---|---|

| Assess Finances | Track income, expenses, debts, net worth | Clear understanding of current situation |

| Set Goals | Short, medium, long-term SMART goals | Direction and purpose |

| Build Emergency Fund | Save 3–6 months of expenses | Financial safety net |

| Budget | Allocate income to needs, wants, savings | Control over spending |

| Manage Debt | Prioritize high-interest debt | Reduce financial stress |

| Invest | Retirement accounts, stocks, REITs | Wealth growth |

| Insurance | Health, life, disability, property | Protect against risks |

| Monitor & Adjust | Review quarterly/annually | Keep plan relevant and effective |

Frequently Asked Questions (FAQs)

Q: How much should I allocate to savings initially?

Even 10–20% of your income can build a solid foundation. Adjust as income and expenses change.

Q: Can I start a financial plan if I have debt?

Yes. Include debt repayment in your plan alongside saving and investing strategies.

Q: How do I stay disciplined with budgeting?

Automate savings, track spending, and set reminders for regular financial reviews.

Q: How often should I review my financial plan?

At least quarterly, or whenever significant life changes occur, such as a new job, relocation, or family growth.

Q: Is an emergency fund more important than investing?

Yes, initially. A fund provides a safety net that protects investments from being liquidated in emergencies.

Final Thoughts

Creating a financial plan from scratch may seem daunting, but breaking it into actionable steps makes it achievable. By assessing your finances, setting clear goals, building an emergency fund, budgeting, managing debt, investing wisely, and protecting yourself with insurance, you can build a comprehensive plan that supports long-term stability and growth.