Your 30s are a critical decade for building financial independence. Income usually becomes more stable, career paths clearer, and financial responsibilities increase. This phase offers a powerful opportunity to create wealth, eliminate financial stress, and design a future where money works for you instead of controlling your choices.

This article explains practical strategies for financial independence planning in your 30s, focusing on smart saving, investing, risk management, and long-term thinking.

What Is Financial Independence?

Financial independence means having enough assets and income to cover your living expenses without relying on active employment. It does not necessarily mean retiring early; it means having control over your financial choices.

Key components include:

-

Sustainable income streams

-

Controlled expenses

-

Strategic investing

-

Strong financial habits

Your 30s provide the ideal balance of time, earning potential, and financial awareness to work toward independence.

Why Your 30s Matter for Financial Independence

The actions you take in your 30s have a long-lasting impact due to the power of compounding and career growth.

Advantages of starting in your 30s:

-

Higher earning capacity than your 20s

-

More financial discipline

-

Clearer life goals

-

Enough time to recover from mistakes

Delaying planning can make financial independence harder to achieve later.

Assess Your Financial Foundation

Before building wealth, ensure your financial base is stable.

Review the following areas:

-

Income consistency

-

Monthly expenses

-

Existing debts

-

Savings and emergency funds

-

Insurance coverage

A strong foundation supports aggressive wealth-building strategies without unnecessary risk.

Control Lifestyle Inflation

As income rises, spending often increases automatically. This can slow progress toward financial independence.

Ways to manage lifestyle inflation:

-

Increase savings alongside income

-

Avoid unnecessary upgrades

-

Focus on value, not status

-

Maintain intentional spending habits

Living below your means accelerates wealth creation.

Build a Robust Emergency Fund

An emergency fund protects progress during unexpected events such as job loss or medical issues.

Recommended approach:

-

Save 6 months of essential expenses

-

Keep funds easily accessible

-

Replenish after use

A strong emergency fund allows you to invest confidently without fear of short-term disruptions.

Eliminate High-Interest Debt

Debt, especially high-interest debt, is a major obstacle to financial independence.

Debt reduction strategies:

-

Prioritize high-interest loans

-

Avoid new unnecessary debt

-

Refinance when possible

-

Make consistent extra payments

Reducing debt frees up cash flow for saving and investing.

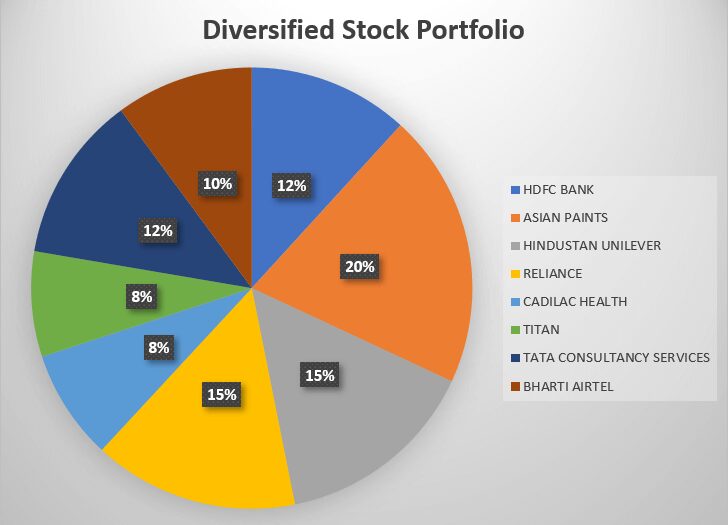

Invest Aggressively but Wisely

Your 30s offer enough time to handle moderate risk while benefiting from long-term growth.

Smart investing principles:

-

Invest consistently

-

Diversify across asset classes

-

Focus on long-term returns

-

Avoid emotional decisions

Balancing growth and stability ensures steady progress toward independence.

Diversify Income Streams

Relying on a single income source increases risk. Multiple income streams improve stability and speed up wealth building.

Examples include:

-

Freelancing or consulting

-

Business ownership

-

Dividend income

-

Rental income

Income diversification protects progress during economic changes.

Plan for Economic Uncertainty

Economic cycles are unavoidable. Preparing for instability strengthens your financial independence strategy.

Understanding How to Manage Money During Economic Uncertainty helps you adjust spending, protect investments, and maintain confidence during unpredictable periods.

Preparedness ensures setbacks do not derail long-term goals.

Set Clear Financial Independence Goals

Clear goals provide direction and motivation.

Examples:

-

Target net worth by age 40

-

Desired passive income level

-

Retirement lifestyle expectations

-

Timeline for debt freedom

Defined goals make progress measurable and actionable.

Comparison Table: Financial Priorities in Your 30s

| Priority | Importance Level | Purpose |

|---|---|---|

| Emergency fund | Very High | Stability |

| Debt elimination | High | Cash flow |

| Investing | Very High | Wealth growth |

| Income diversification | High | Risk reduction |

| Insurance | Medium | Protection |

| Lifestyle control | High | Sustainability |

Protect Your Assets With Insurance

Insurance shields your progress from unexpected financial shocks.

Important coverage to consider:

-

Health insurance

-

Life insurance

-

Disability insurance

-

Property insurance

Protection is an essential part of long-term planning.

Track Progress and Adjust Regularly

Financial independence planning is not static. Regular reviews ensure your strategy stays aligned with goals.

Best practices:

-

Review finances quarterly

-

Adjust investments annually

-

Update goals as life changes

-

Monitor net worth growth

Consistency and flexibility lead to better outcomes.

Maintain the Right Mindset

Financial independence is a long-term journey that requires patience and discipline.

Mindset shifts to adopt:

-

Focus on progress, not perfection

-

Accept temporary sacrifices

-

Stay committed during market downturns

-

Avoid comparison with others

A strong mindset is as important as financial strategy.

Frequently Asked Questions (FAQs)

Is it too late to plan for financial independence in your 30s?

No. Your 30s are one of the best decades to start due to income growth and time for compounding.

How much should I save in my 30s?

Aiming to save and invest 20–30% of income is a strong target, depending on expenses and goals.

Should I prioritize investing or debt repayment?

High-interest debt should be addressed first, while still investing consistently if possible.

Can financial independence be achieved without a high salary?

Yes. Consistent saving, controlled spending, and smart investing matter more than income alone.

How long does financial independence take?

It varies based on income, savings rate, and investment returns, but disciplined planning accelerates the process.

Conclusion

Financial independence planning in your 30s is about using your peak earning years wisely. By controlling expenses, eliminating debt, building emergency savings, investing strategically, and preparing for uncertainty, you create a solid path toward long-term freedom. The decisions you make now shape your financial future for decades to come.